Half of global greenhouse gas emissions are now covered by a 2035 climate pledge following a key UN summit this week, Carbon Brief analysis finds.

China stole the show at the UN climate summit held in New York on 24 September, announcing a pledge to cut greenhouse gas emissions to 7-10% below peak levels by 2035.

However, other major emitters also came forward with new climate-pledge announcements at the event, including the world’s fourth biggest emitter, Russia, and Turkey.

Following the summit, around one-third (63) of countries have now announced or submitted their 2035 climate pledges, known as “nationally determined contributions” (NDCs).

The NDCs are a formal five-yearly requirement under the “ratchet mechanism” of the Paris Agreement, the landmark deal to keep temperatures well-below 2C, with aspirations to keep to 1.5C, by the end of this century.

Nations were meant to have submitted these pledges by 10 February of this year, but around 95% of countries missed this deadline.

UN climate chief Simon Stiell then asked laggard countries to make 2035 pledges by the end of September, so they can be included in a report synthesising countries’ climate progress.

At the summit, many nations shared that they were still working on their NDCs and that they would aim to submit them to the UN before or during COP30 in November.

The map below shows countries that submitted their 2035 pledges by the 10 February deadline (dark blue), after the deadline (blue) and that have now announced their pledge, but not yet submitted it formally to the UN registry (pale blue).

The EU has not yet agreed on a 2035 climate pledge. At the UN climate summit, European Commission president Ursula von der Leyen announced a “statement of intent” to cut emissions somewhere in the range of 66.3-72.5% below 1990 levels by 2035.

She added that the EU would aim to make its formal NDC submission to the UN before COP30 in November.

The world’s second-largest emitter, the US, submitted its 2035 pledge in 2024 under former president Joe Biden.

However, current president Donald Trump has since signed an order to withdraw the country from the Paris Agreement. Therefore, it is now assumed that the US pledge is now void.

More than 100 nations spoke at the UN climate summit, which was held on the margins of the annual UN general assembly in New York.

Some media outlets mistakenly reported that all of these countries “announced” new pledges at the summit.

However, many of the countries speaking at the summit had already submitted their 2035 pledges, or used their slots to promise to do so at a future date.

Carbon Brief reviewed the six hours of footage from the UN climate summit to get a clear picture of which countries announced new 2035 pledges during the event.

Countries that made new NDC target announcements during the event included China, Russia, Turkey, Palau, Tuvalu, Kyrgyzstan, Peru, São Tomé and Príncipe, Fiji, Bangladesh and Eritrea. (Tuvalu has since submitted its NDC to the UN.)

These countries together represent 36% of global greenhouse gas emissions, according to Carbon Brief analysis. (It is worth noting that China alone accounts for 29% of emissions.)

Some 53 countries have already submitted their 2035 climate pledges to the UN Framework Convention on Climate Change (UNFCCC). These nations account for 14% of global greenhouse gas emissions.

Therefore, countries that have either announced or submitted their 2035 climate pledges now represent half of global emissions, according to Carbon Brief analysis. (The 50% figure excludes the US and the EU for the reasons outlined above.)

Despite the new announcements, two-thirds of nations have still not submitted their 2035 climate pledges, according to Carbon Brief analysis.

This includes major emitters, such as India, Indonesia and Mexico.

According to the Hindu, India plans to submit its 2035 climate pledge at the beginning of COP30 on 10 November.

Both Mexico and Indonesia spoke at the UN climate summit. Mexico said it was “still consulting industries” about its proposed target, while Indonesia made no mention of when it might submit its NDC.

Many other nations appearing at the summit made promises to submit their 2035 climate pledges by COP30.

This might mean that many nations miss the end of September deadline set by UN climate chief Simon Stiell to be included in an upcoming NDC synthesis report.

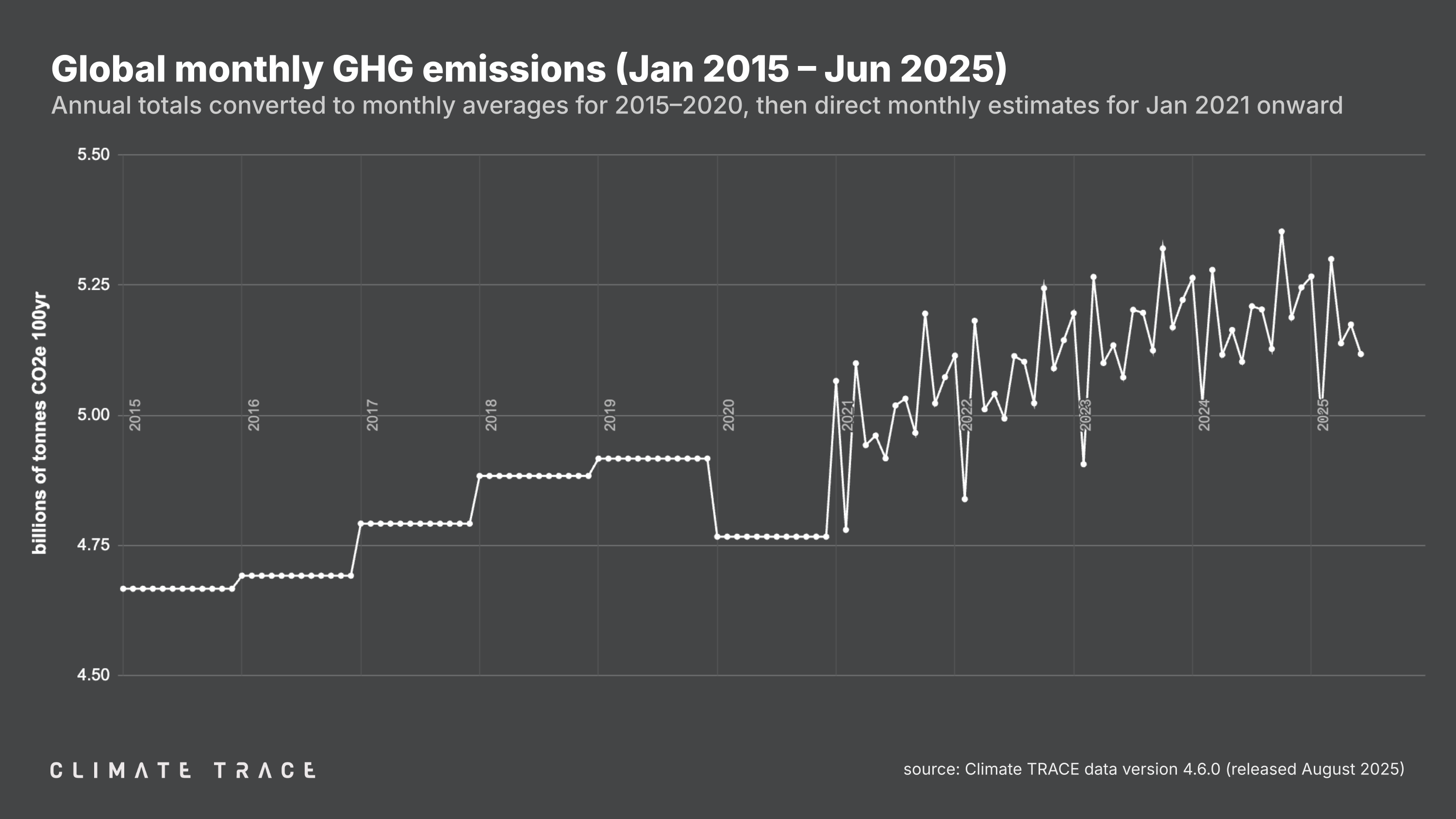

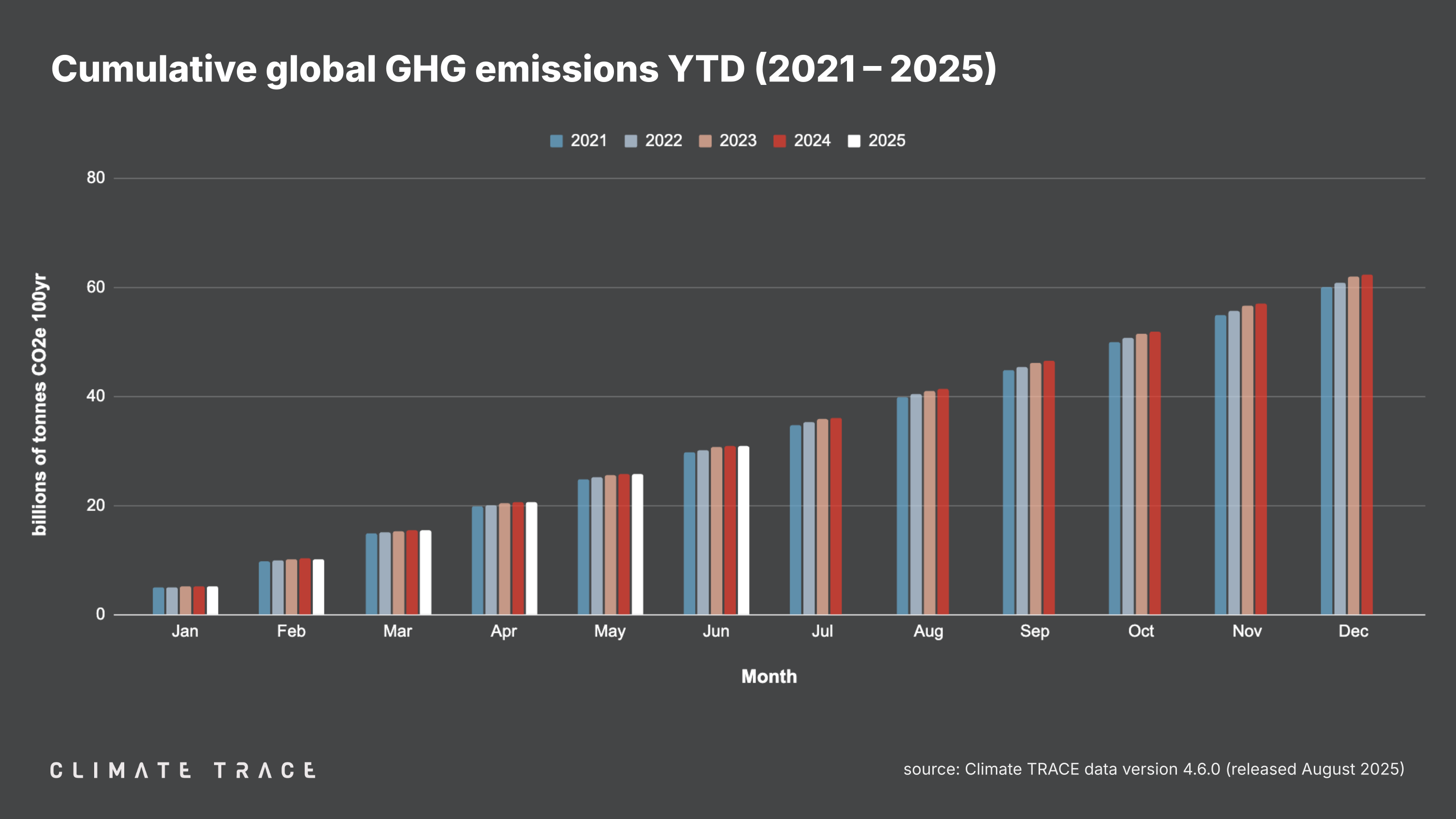

August 28, 2025 – Today, Climate TRACE reported that total global emissions in the first half of 2025 are 30.99 billion tonnes CO₂e. This is 0.13% higher than emissions were in the first half of 2024. Global greenhouse gas emissions for the month of June 2025 totaled 5.12 billion tonnes CO₂e. This represents an increase of 0.29% vs. June 2024. Global methane emissions in June 2025 were 34.82 million tonnes CH₄, an increase of 0.49% vs. June 2024.

Data tables summarizing emissions totals for June 2025 by sector, country, and top 100 urban areas are available for download here.

Lookback: Global Greenhouse Gas Emissions for the First Half of 2025

In the first half of 2025, the sector driving the most growth in emissions was fossil fuel operations, where emissions rose by 1.5% (an increase of 77.65 million tonnes of CO₂e). The United States accounted for more than half of that increase. Manufacturing emissions also rose in the first half of 2025, growing by 0.3% (an increase of 18.75 million tonnes of CO₂e), led by increases in India, Vietnam, Indonesia, and Brazil.

Meanwhile, global power sector emissions saw the biggest decline in the first half of 2025, falling by 0.8% (a decrease of 60.27 million tonnes of CO₂e), driven almost entirely by declines in China and India, where power emissions were 1.7% lower and 0.8% lower than their totals in the first half of 2024, respectively.

The first half of 2025 shows small but positive progress on decarbonization in China, Mexico, and Australia. China’s emissions decreased 45.37 million tonnes CO₂e, or 0.51% compared to the first half of 2024. Mexico’s emissions decreased 7.78 million tonnes CO₂e, or 1.71% compared to the first half of 2024. Australia’s emissions decreased 6.56 million tonnes CO₂e, or 1.51% compared to the first half of 2024. However, some of the world’s other major emitting economies, including the United States, India, the EU, Indonesia, and Brazil, saw emissions rise in the first half of 2025.

– United States emissions increased by 48.57 million tonnes CO₂e, or 1.43% compared to the first half of 2024;

– India emissions increased by 4.44 million tonnes CO₂e, or 0.21% compared to the first half of 2024;

– European Union emissions increased by 2.90 million tonnes CO₂e, or 0.15% compared to the first half of 2024.

– Indonesia emissions increased by 3.06 million tonnes CO₂e, or 0.39% compared to the first half of 2024;

– Brazil emissions increased by 9.84 million tonnes CO₂e, or 1.24% compared to the first half of 2024.

Greenhouse Gas Emissions by Country: June 2025

Climate TRACE’s preliminary estimate of June 2025 emissions in China, the world’s top emitting country, is 1.46 billion tonnes CO₂e — an increase of 0.92 million tonnes of CO₂e or 0.06% vs. June 2024.

Of the other top five emitting countries:

– United States emissions increased by 4.89 million tonnes CO₂e, or 0.86% year over year;

– India emissions declined by 0.11 million tonnes CO₂e, or 0.03% year over year;

– Russia emissions increased by 0.95 million tonnes CO₂e, or 0.38% year over year;

– Indonesia emissions increased by 0.43 million tonnes CO₂e, or 0.33% year over year.

In the EU, which as a bloc would be the fourth largest source of emissions in June 2025, emissions declined by 1.80 million tonnes CO₂e compared to June 2024, or 0.58%.

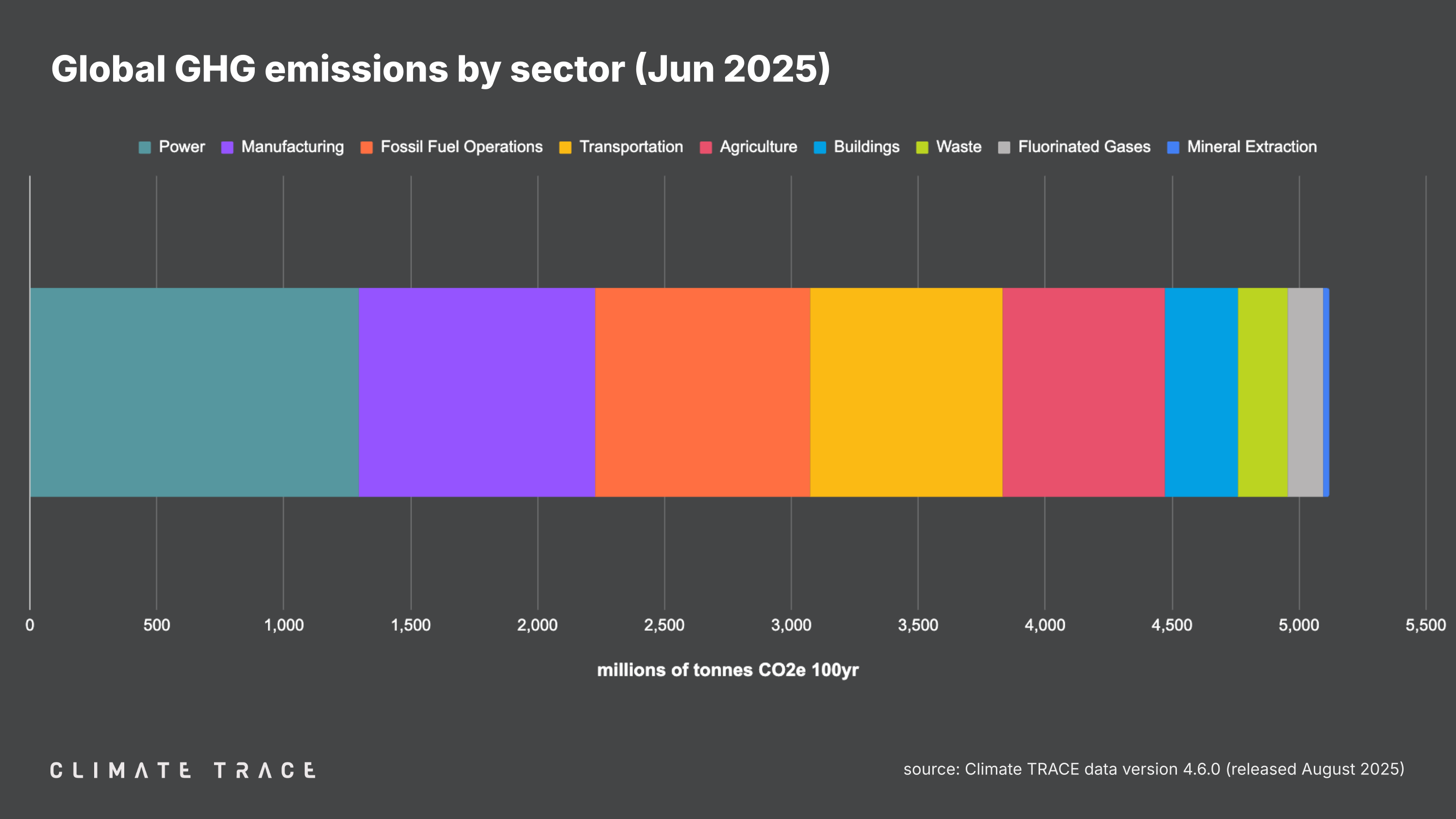

Greenhouse Gas Emissions by Sector: June 2025

Greenhouse gas emissions increased in June 2025 vs. June 2024 in fossil fuel operations, manufacturing, transportation, and waste, and decreased in power. Fossil fuel operations saw the greatest change in emissions year over year, with emissions increasing by 1.85% as compared to June 2024.

– Agriculture emissions were 641.40 million tonnes CO₂e, unchanged vs. June 2024;

– Buildings emissions were 285.59 million tonnes CO₂e, unchanged vs. June 2024;

– Fluorinated gases emissions were 137.71 million tonnes CO₂e, unchanged vs. June 2024;

– Fossil fuel operations emissions were 846.19 million tonnes CO₂e, a 1.85% increase vs. June 2024;

– Manufacturing emissions were 929.05 million tonnes CO₂e, a 0.02% increase vs. June 2024;

– Mineral extraction emissions were 23.22 million tonnes CO₂e, unchanged vs. June 2024;

– Power emissions were 1,297.34 million tonnes CO₂e, a 0.56% decrease vs. June 2024;

– Transportation emissions were 759.10 million tonnes CO₂e, a 0.77% increase vs. June 2024;

– Waste emissions were 197.77 million tonnes CO₂e, a 0.26% increase vs. June 2024.

Greenhouse Gas Emissions by City: June 2025

The urban areas with the highest total greenhouse gas emissions in June 2025 were Shanghai, China; Tokyo, Japan; New York, United States; Houston, United States; and Los Angeles, United States.

The urban areas with the greatest increase in absolute emissions in June 2025 as compared to June 2024 were Pittsburgh, United States; Xinyu, China; Tokyo, Japan; Baotou, China; and Algeciras, Spain. Those with the largest absolute emissions decline between this June and last June were Leipzig, Germany; Anqing, China; Duren, Germany; Houston, United States; and Anchorage, United States.

The urban areas with the greatest increase in emissions as a percentage of their total emissions were Kombissiri, Burkina Faso; Gambat, Pakistan; Bitilta Zebraro, Ethiopia; UNNAMED, Sudan; and Oviedo, Spain. Those with the greatest decrease by percentage were Leipzig, Germany; Duren, Germany; Wolfsburg, Germany; Atebubu, Ghana; and Evansville, United States.

RELEASE NOTES

Revisions to existing Climate TRACE data are common and expected. They allow us to take the most up-to-date and accurate information into account. As new information becomes available, Climate TRACE will update its emissions totals (potentially including historical estimates) to reflect new data inputs, methodologies, and revisions.

With the addition of June 2025 data, the Climate TRACE database is now updated to version V4.6.0. This release incorporates the most recent FAOSTAT and CEDS data in applicable sectors. The release also reflects updated methodology for non-GHG emissions from glass, cement, and lime production; the addition of N2O emissions across agriculture subsectors and additional refinements to agriculture emissions factors; updated North America and Europe data for Q4 2024 in petrochemicals and oil and gas refining; updated methodology and data for cement and steel production to reflect updated emissions factors; and the addition of 56 steel plants to our database.

A detailed description of data updates is available in our changelog here.

To learn more about what is included in our monthly data releases and for frequently asked questions, click here. All methodologies for Climate TRACE data estimates are available to view and download here. For any further technical questions about data updates, please contact: coalition@ClimateTRACE.org.

To sign up for monthly updates from Climate TRACE, click here.

Emissions data for July 2025 are scheduled for release on September 25, 2025.

About Climate TRACE

The Climate TRACE coalition was formed by a group of AI specialists, data scientists, researchers, and nongovernmental organizations. Current members include Carbon Yield; CTrees; Duke University’s Nicholas Institute for Energy, Environment & Sustainability; Earth Genome; Former Vice President Al Gore; Global Energy Monitor; Hypervine.io; Johns Hopkins University Applied Physics Lab; OceanMind; RMI; TransitionZero; and WattTime. Climate TRACE is also supported by more than 100 other contributing organizations and researchers, including key data and analysis contributors: Arboretica, Carnegie Mellon University’s CREATE Lab, Global Fishing Watch/emLab, Michigan State University, Open Supply Hub, and University of Malaysia Terengganu. For more information about the coalition and a list of contributors, click here.

Media Contacts

Fae Jencks and Nikki Arnone for Climate TRACE

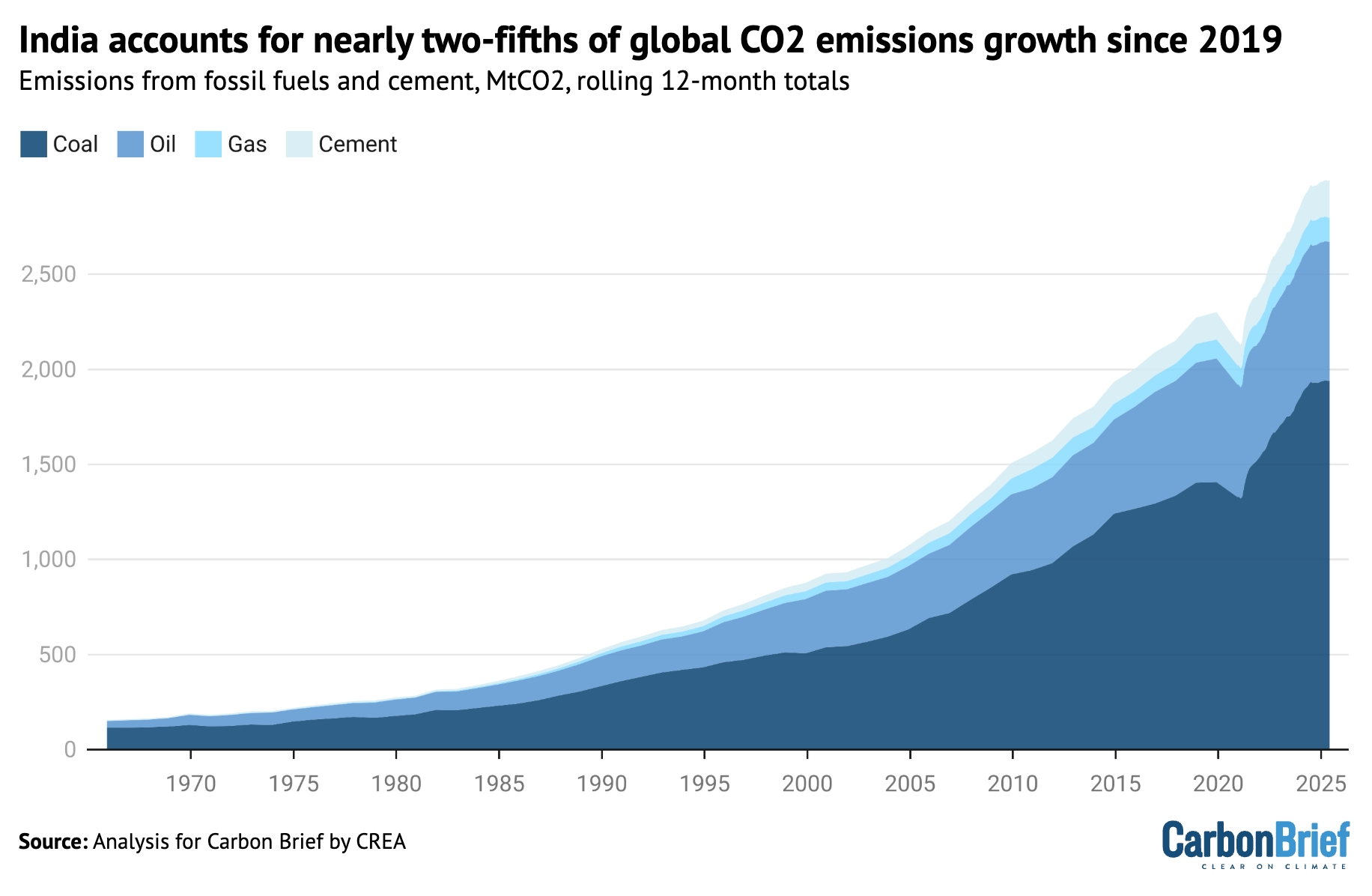

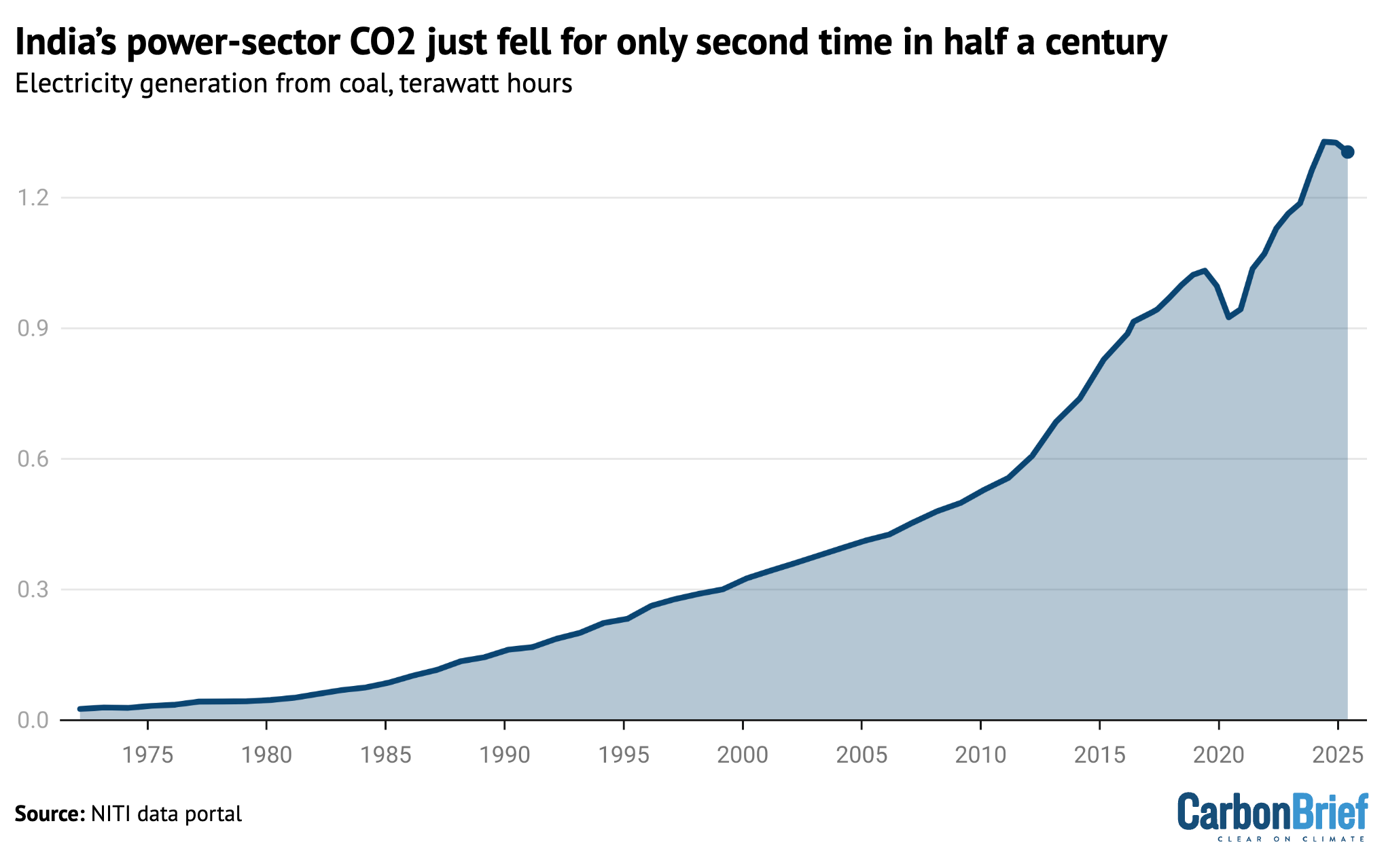

India’s carbon dioxide (CO2) emissions from its power sector fell by 1% year-on-year in the first half of 2025 and by 0.2% over the past 12 months, only the second drop in almost half a century.

As a result, India’s CO2 emissions from fossil fuels and cement grew at their slowest rate in the first half of the year since 2001 – excluding Covid – according to new analysis for Carbon Brief.

The analysis is the first of a regular new series covering India’s CO2 emissions, based on monthly data for fuel use, industrial production and power output, compiled from numerous official sources.

(See the regular series on China’s CO2 emissions, which began in 2019.)

Other key findings on India for the first six months of 2025 include:

The analysis also shows that emissions from India’s power sector could peak before 2030, if clean-energy capacity and electricity demand grow as expected.

The future of CO2 emissions in India is a key indicator for the world, with the country – the world’s most populous – having contributed nearly two-fifths of the rise in global energy-sector emissions growth since 2019.

In 2024, India was responsible for 8% of global energy-sector CO2 emissions, despite being home to 18% of the world’s population, as its per-capita output is far below the world average.

However, emissions have been growing rapidly, as shown in the figure below.

The country contributed 31% of global energy-sector emissions growth in the decade to 2024, rising to 37% in the past five years, due to a surge in the three-year period from 2021-23.

More than half of India’s CO2 output comes from coal used for electricity and heat generation, making this sector the most important by far for the country’s emissions.

The second-largest sector is fossil fuel use in industry, which accounts for another quarter of the total, while oil use for transport makes up a further eighth of India’s emissions.

India’s CO2 emissions from fossil fuels and cement grew by 8% per year from 2019 to 2023, quickly rebounding from a 7% drop in 2020 due to Covid.

Before the Covid pandemic, emissions growth had averaged 4% per year from 2010 to 2019, but emissions in 2023 and 2024 rose above the pre-pandemic trendline.

This was despite a slower average GDP growth rate from 2019 to 2024 than in the preceding decade, indicating that the economy became more energy- and carbon-intensive. (For example, growth in steel and cement outpaced the overall rate of economic growth.)

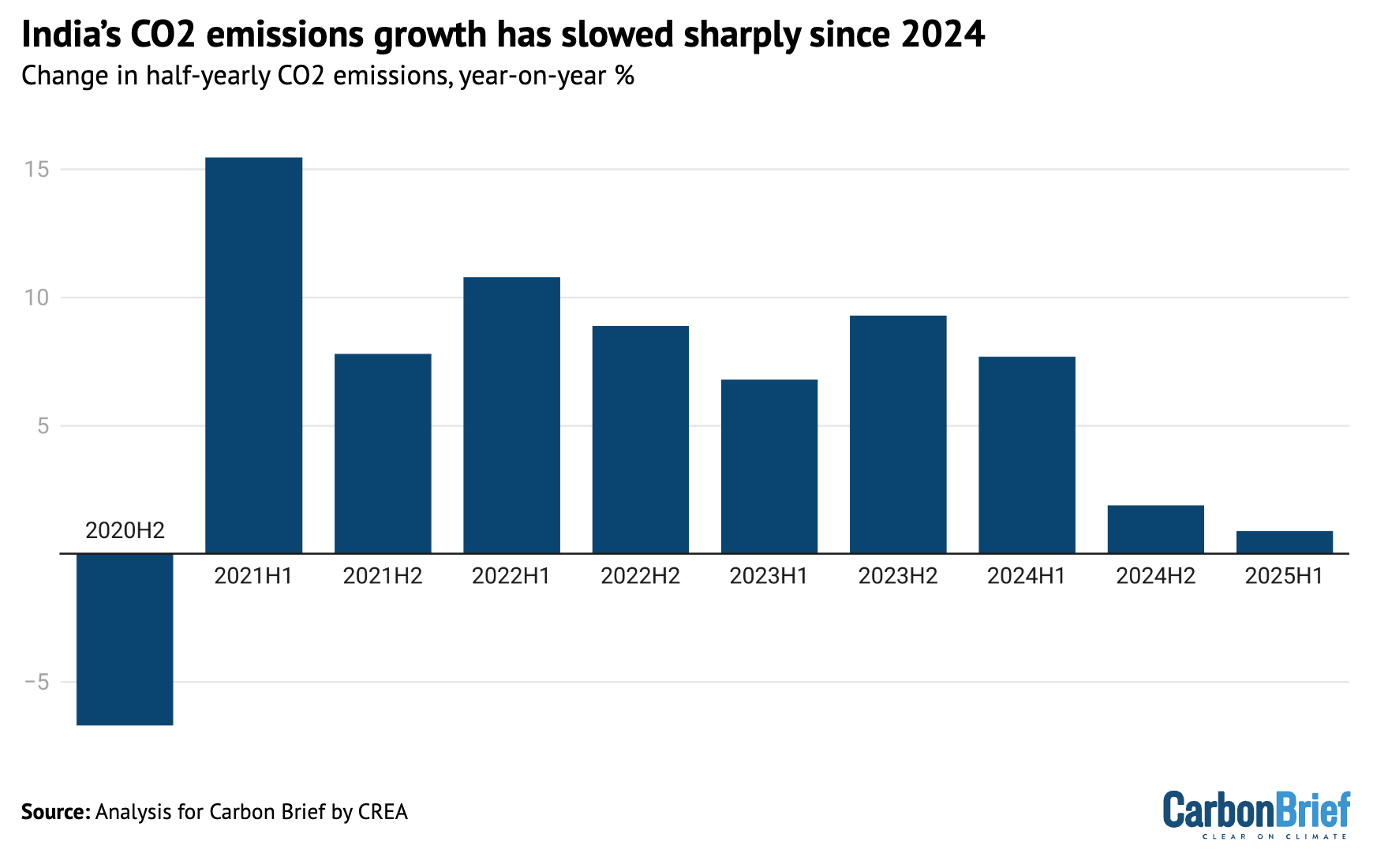

A turnaround came in the second half of 2024, when emissions only increased by 2% year-on-year, slowing down to 1% in the first half of 2025, as seen in the figure below.

The largest contributor to the slowdown was the power sector, which was responsible for 60% of the drop in emissions growth rates, when comparing the first half of 2025 with the years 2021-23.

Oil demand growth slowed sharply as well, contributing 20% of the slowdown. The only sectors to keep growing their emissions in the first half of 2025 were steel and cement production.

Another 20% of the slowdown was due to a reduction in coal and gas use outside the power, steel and cement sectors. This comprises construction, industries such as paper, fertilisers, chemicals, brick kilns and textiles, as well as residential and commercial cooking, heating and hot water.

This is all shown in the figure below, which compares year-on-year changes in emissions during the second half of 2024 and the first half of 2025, with the average for 2021-23.

Power sector emissions fell by 1% in the first half of 2025, after growing 10% per year during 2021-23 and adding more than 50m tonnes of CO2 (MtCO2) to India’s total every six months.

Oil product use saw zero growth in the first half of 2025, after rising 6% per year in 2021-23.

In contrast, emissions from coal burning for cement and steel production rose by 10% and 7%, respectively, while coal use outside of these sectors fell 2%.

Gas consumption fell 7% year-on-year, with reductions across the power and industrial sectors as well as other users. This was a sharp reversal of the 5% average annual growth in 2021-23.

The most striking shift in India’s sectoral emissions trends has come in the power sector, where coal consumption and CO2 emissions fell 0.2% in the 12 months to June and 1% in the first half of 2025, marking just the second drop in half a century, as shown in the figure below.

The reduction in coal use comes after more than a decade of break-neck growth, starting in the early 2010s and only interrupted by Covid in 2020. It also comes even as the country plans large amounts of new coal-fired generating capacity.

In the first half of 2025, total power generation increased by 9 terawatt hours (TWh) year-on-year, but fossil power generation fell by 29TWh, as output from solar grew 17TWh, from wind 9TWh, from hydropower by 9TWh and from nuclear by 3TWh.

Analysis of government data shows that 65% of the fall in fossil-fuel generation can be attributed to lower electricity demand growth, 20% to faster growth in non-hydro clean power and the remaining 15% to higher output at existing hydropower plants.

Slower growth in electricity usage was largely due to relatively mild temperatures and high rainfall, in contrast to the heatwaves of 2024. A slowdown in industrial sectors in the second quarter of the year also contributed.

In addition, increased rainfall drove the jump in hydropower generation. India received 42% above-normal rainfall from March to May 2025. (In early 2024, India’s hydro output had fallen steeply as a result of “erratic rainfall”.)

Lower temperatures and this abundant rainfall reduced the need for air conditioning, which is responsible for around 10% of the country’s total power demand. In the same period in 2024, demand surged due to record heatwaves and higher temperatures across the country.

The growth in clean-power generation was buoyed by the addition of a record 25.1GW of non-fossil capacity in the first half of 2025. This was a 69% increase compared with the previous period in 2024, which had also set a record.

Solar continues to dominate new installations, with 14.3GW of capacity added in the first half of the year coming from large scale solar projects and 3.2GW from solar rooftops.

Solar is also adding the majority of new clean-power output. Taking into account the average capacity factor of each technology, solar power delivered 62% of the additional annual generation, hydropower 16%, wind 13% and nuclear power 8%.

The new clean-energy capacity added in the first half of 2025 will generate record amounts of clean power. As shown in the figure below, the 50TWh per year from this new clean capacity is approaching the average growth of total power generation.

(When clean-energy growth exceeds total demand growth, generation from fossil fuels declines.)

India is expected to add another 16-17GW of solar and wind in the second half of 2025. Beyond this year, strong continued clean-energy growth is expected, towards India’s target for 500GW of non-fossil fuel capacity by 2030 (see below).

The first half of 2025 also saw a significant slowdown in India’s oil demand growth. After rising by 6% a year in the three years to 2023, it slowed to 4% in 2024 and zero in the first half of 2025.

The slowdown in oil consumption overall was predominantly due to slower growth in demand for diesel and “other oil products”, which includes bitumen.

In the first quarter of 2025, diesel demand actually fell, due to a decline in industrial activity, limited weather-related mobility and – reportedly – higher uptake of vehicles that run on compressed natural gas (CNG), as well as electricity (EVs).

Diesel demand growth increased in March to May, but again declined in June because of early and unusually severe monsoon rains in India, leading to a slowdown in industrial and mining activities, disrupted supply-chains and transport of raw material, goods and services.

The severe rains also slowed down road construction activity, which in turn curtailed demand for transportation, construction equipment and bitumen.

Weaker diesel demand growth in 2024 had reflected slower growth in economic activity, as growth rates in the industrial and agricultural sectors contracted compared to previous years.

Another important trend is that EVs are also cutting into diesel demand in the commercial vehicles segment, although this is not yet a significant factor in the overall picture.

EV adoption is particularly notable in major metropolitan cities and other rapidly emerging urban centres and in the logistics sector, where they are being preferred for short haul rides over diesel vans or light commercial vehicles.

EVs accounted for only 7.6% of total vehicle sales in the financial year 2024-25, up 22.5% year-on-year, but still far from the target of 30% by 2030.

However, any significant drop in diesel demand will be a function of adoption of EV for long-haul trucks, which account for 32% of the total CO2 emissions from the transport sector. Only 280 electric trucks were sold in 2024, reported NITI Aayog.

Trucks remain the largest diesel consumers. Moreover, truck sales grew 9.2% year-on-year in the second quarter of 2025, driven in part by India’s target of 75% farm mechanisation by 2047. This sales growth may outweigh the reduction in diesel demand due to EVs. Subsidies for electric tractors have seen some pilots, but demand is yet to take off.

Apart from diesel, petrol demand growth continued in the first half of 2025 at the same rate as in earlier years. Modest year-on-year growth of 1.3% in passenger vehicle sales could temper future increases in petrol demand, however. This is a sharp decline from 7.5% and 10% growth rates in sales in the same period in 2024 and 2023.

Furthermore, EVs are proving to be cheaper to run than petrol for two- and three-wheelers, which may reduce the sale of petrol vehicles in cities that show policy support for EV adoption.

As already noted, steel and cement were the only major sectors of India’s economy to see an increase in emissions growth in the first half of 2025.

While they were only responsible for around 12% of India’s total CO2 emissions from fossil fuels and cement in 2024, they have been growing quickly, averaging 6% a year for the past five years.

The growth in emissions accelerated in the first half of 2025, as cement output rose 10% and steel output 7%, far in excess of the growth in economic output overall.

Steel and cement growth accelerated further in July. A key demand driver is government infrastructure spending, which tripled from 2019 to 2024.

In the second quarter of 2025, the government’s capital expenditure increased 52% year-on-year. albeit from a low base during last year’s elections. This signals strong growth in infrastructure.

The government is targeting domestic steel manufacturing capacity of 300m tonnes (Mt) per year by 2030, from 200Mt currently, under the National Steel Policy 2017, supported by financial incentives for firms that meet production targets for high quality steel.

The government also imposed tariffs on steel imports in April and stricter quality standards for imports in June, in order to boost domestic production.

Government policies such as Pradhan Mantri Awas Yojna – a “housing for all” initiative under which 30m houses are to be built by FY30 – is further expected to lift demand for steel and cement.

The automotive sector in India is expected to grow at a fast pace, with sales expected to reach 7.5m units for passenger vehicle and commercial vehicle segments from 5.1m units in 2023, in addition to rapid growth in electric vehicles. This can be expected to be another key driver for growth of the steel sector, as 900 kg of steel is used per vehicle.

Without stringent energy efficiency measures and the adoption of cleaner fuel, the expected growth in steel and cement production could drive significant emissions growth from the sector.

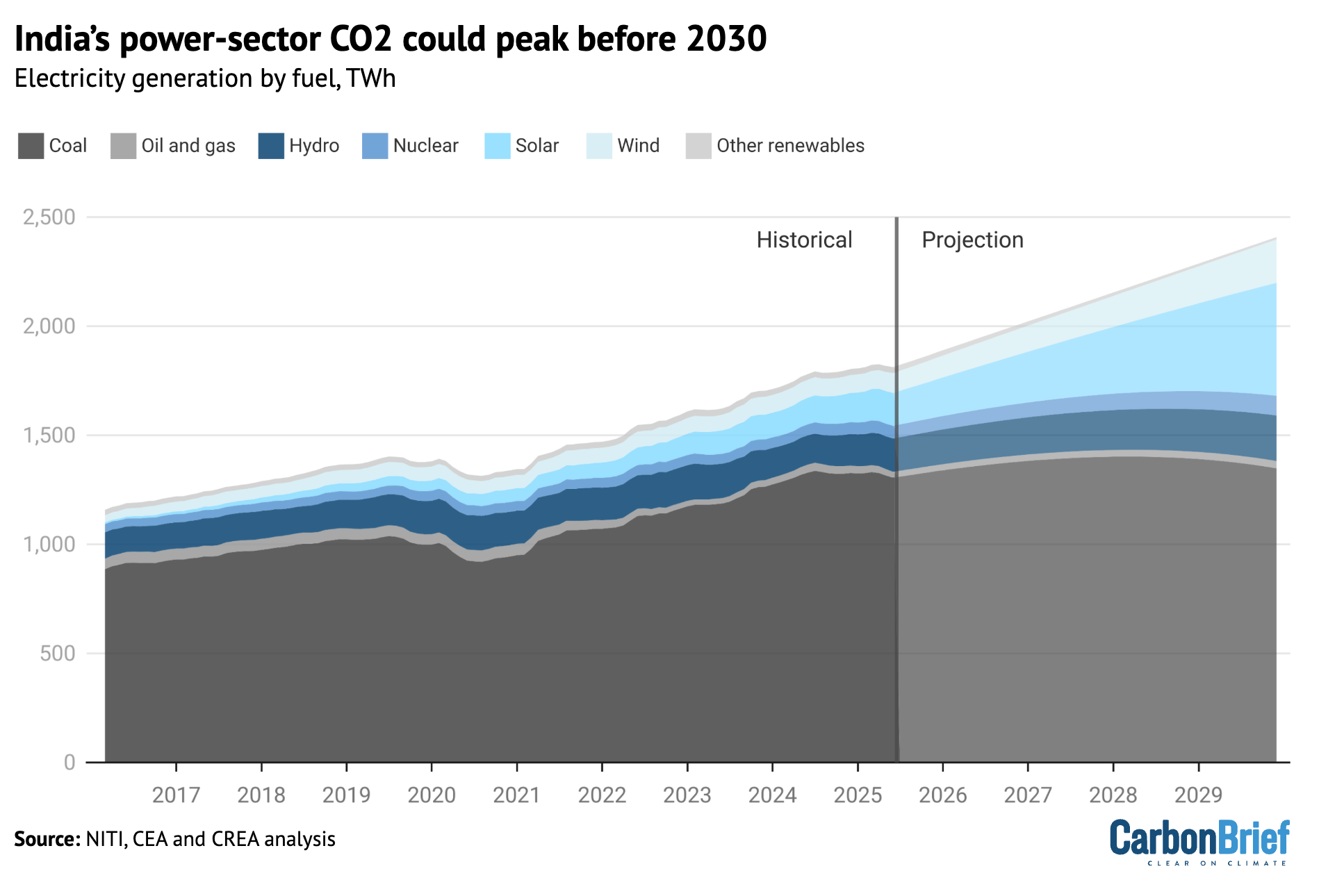

Looking beyond this year, the analysis shows that CO2 from India’s power sector could peak before 2030, having previously been the main driver of emissions growth.

To date, India’s clean-energy additions have been lagging behind the growth in total electricity demand, meaning fossil-fuel demand and emissions from the sector have continued to rise.

However, this dynamic looks likely to change. In 2021, India set a target of having 500GW of non-fossil power generation capacity in place by 2030. Progress was slow at first, so meeting the target implies a substantial acceleration in clean-energy additions.

The country has been laying the groundwork for such an acceleration.

There was 234GW of renewable capacity in the pipeline as of April 2025, according to the Ministry of New and Renewable Energy. This includes 169GW already awarded contracts, of which 145GW is under construction, and an additional 65GW put out to tender. There is also 5.2GW of new nuclear capacity under construction.

If all of this is commissioned by 2030, then total non-fossil capacity would increase to 482GW, from 243GW at the end of June 2025, leaving a gap of just 18GW to be filled with new projects.

When the non-fossil capacity target was set in 2021, CREA assessed that the target would suffice to peak demand for coal in power generation before 2030. This assessment remains valid and is reinforced by the latest Central Electricity Authority (CEA) projection for the country’s “optimal power mix” in 2030, shown in the figure below.

In the CEA’s projection, the share of non-fossil power generation rises to 44% in the 2029-30 fiscal year, up from 25% in 2024-25. From 2025 to 2030, power demand growth, averaging 6% per year, is entirely covered from clean sources.

To accomplish this, the growth in non-fossil power generation would need to accelerate over time, meaning that towards the end of the decade, the growth in clean power supply would clearly outstrip demand growth overall – and so power generation from fossil fuels would fall.

While coal-power generation is expected to flatline, large amounts of new coal-power capacity is still being planned, because of the expected growth in peak electricity demand.

The post-Covid increase in electricity demand has given rise to a wave of new coal power plant proposals. Recent plans from the government target an increase in coal-power capacity by another 80-100GW by 2030-32, with 35GW already under construction as of July 2025.

The rationale for this is the increase in peak electricity loads, associated in particular with worsening heatwaves and growing use of air conditioning. The increase might yet prove unneeded.

Analysis by CREA shows that solar and wind are making an increasing contribution to meeting peak loads. This contribution will increase with the roll-out of solar power with integrated battery storage, the cost of which fell by 50-60% from 2023 to 2025.

The latest auction held in India saw solar power with battery storage bidding at prices, per unit of electricity generation, that were lower than the cost of new coal power.

This creates the opportunity to accelerate the decarbonisation of India’s power sector, by reducing the need for thermal power capacity.

The clean-energy buildout has made it possible for India to peak its power-sector emissions within the next few years, if contracted projects are built, clean-energy growth is maintained or accelerated beyond 2030 and demand growth remains within the government’s projections.

This would be a major turning point, as the power sector has been responsible for half of India’s recent emissions growth. In order to peak its emissions overall, however, India would still need to take further action to address CO2 from industry and transport.

With the end-of-September 2025 deadline nearing, India has yet to publish its international climate pledge (nationally determined contribution, NDC) for 2035 under the Paris Agreement, meaning its future emissions path, in the decades up to its 2070 net-zero goal, remains particularly uncertain.

The country is expected to easily surpass the headline climate target from its previous NDC, of cutting the emissions intensity of its economy to 45% below 2005 levels by 2030. As such, this goal is “unlikely to drive real world emission reductions”, according to Climate Action Tracker.

In July of this year, it met a 2030 target for 50% of installed power generating capacity to be from non-fossil sources, five years early.

This analysis is based on official monthly data for fuel consumption, industrial production and power generation from different ministries and government institutes.

Coal consumption in thermal power plants is taken from the monthly reports downloaded from the National Power Portal of the Ministry of Power. The data is compiled for the period January 2019 until June 2025. Power generation and capacity by technology and fuel on a monthly basis are sourced from the NITI data portal.

Coal use at steel and cement plants, as well as process emissions from cement production, are estimated using production indices from the Index of Eight Core Industries released monthly by the Office of Economic Adviser, assuming that changes in emissions follow production volumes.

These production indices were used to scale coal use by the sectors in 2022. To form a basis for using the indices, monthly coal consumption data for 2022 was constructed for the sectors using the annual total coal consumption reported in IEA World Energy Balances and monthly production data in a paper by Robbie Andrew, on monthly CO2 emission accounting for India.

Annual cement process emissions up to 2024 were also taken from Robbie Andrew’s work and scaled using the production indices. This approach better approximated changes in energy use and emissions reported in the IEA World Energy Balances, than did the amounts of coal reported to have been dispatched to the sectors, showing that production volumes are the dominant driver of short-term changes in emissions.

For other sectors, including aluminium, auto, chemical and petrochemical, paper and plywood, pharmaceutical, graphite electrode, sugar, textile, mining, traders and others, coal consumption is estimated based on data on despatch of domestic and imported coal to end users from statistical reports and monthly reports by the Ministry of Coal, as consumption data is not available.

The difference between consumption and dispatch is stock changes, which are estimated by assuming that the changes in coal inventories at end user facilities mirror those at coal mines, with end user inventories excluding power, steel and cement assumed to be 70% of those at coal mines, based on comparisons between our data and the IEA World Energy Balances.

Stock changes at mines are estimated as the difference between production at and despatch from coal mines, as reported by the Ministry of Coal.

In the case of the second quarter of the year 2025, data on domestic coal has been taken from the monthly reports by the Ministry of Coal. The regular data releases on coal imports have not taken place for the second quarter of 2025, for unknown reasons, so data was taken from commercial data providers Coal Hub and mjunction services ltd.

Product-wise petroleum product consumption data, as well as gas use by sector, was downloaded from the Petroleum Planning and Analysis Cell of the Ministry of Petroleum & Natural Gas.

As the fuel dispatch and consumption data is reported as physical volumes, calorific values are taken from IEA’s World Energy Balance and CO2 emission factors from 2006 IPCC Guidelines for National Greenhouse Gas Inventories.

Calorific values are assigned separately to different fuel types, including domestic and imported coal, anthracite and coke, as well as petrol, diesel and several other oil products.

Cleveland has big ambitions to reduce its planet-warming emissions. But a massive steelmaking facility run by Cleveland-Cliffs, one of Ohio’s major employers, could make it difficult for the city to see those plans through.

The plant emits roughly 4.2 million metric tons of greenhouse gases each year, complicating Cleveland’s effort to achieve net-zero emissions by 2050, according to a report released by advocacy group Industrious Labs this summer. The plant is the city’s largest single source of planet-warming pollution.

Cleveland’s climate action plan is “bold and achievable,” said Hilary Lewis, steel director for Industrious Labs. But “if they want to achieve those goals, they have to take action on this Cleveland Works facility.”

As a major investment decision looms over an aging blast furnace at the facility, it’s unclear whether the company will move to cut its direct greenhouse gas emissions — or opt to reinvest in its existing coal-dependent processes.

Cliffs’ progress in reducing its nationwide emissions earned it recognition as a 2023 Goal Achiever in the Department of Energy’s Better Climate Challenge. As this year began, the company was set to slash emissions even further through projects supported by Biden-era legislation — the Inflation Reduction Act and the 2021 infrastructure law.

Then the Trump administration commenced its monthslong campaign of reneging on funding commitments for clean energy projects, including ones meant to ramp up the production of “green” hydrogen made with renewable energy. In June, Cliffs’ CEO Lourenco Goncalves backed away from a federally funded project to convert its Middletown Works in southwestern Ohio to produce green steel, saying there wouldn’t be a sufficient supply of hydrogen for the plant.

To Lewis, coauthor of the Industrious Labs report, that’s a weak excuse, because hydrogen production by other companies would have ramped up to supply the facility. “[Cliffs was] going to need so much hydrogen that they would be creating the demand,” she said.

Meanwhile, Cliffs’ Cleveland Works continues to spew emissions that drive climate change and harm human health. Industrious Labs’ modeling estimates that pollution from Cleveland Works is responsible for up to 39 early deaths per year, more than 1,700 lost work days, and more than 9,000 asthma cases. Cleveland ranks as the country’s fifth-worst city for people with asthma, according to the Asthma and Allergy Foundation of America.

Cleveland Works’ Blast Furnace #6 is a hulking vessel that removes impurities from iron ore by combining it with limestone and coke, a form of coal that burns at very high temperatures. Industrious Labs’ report notes the unit’s lining is nearing the end of its useful life.

To Industrious Labs, this presents an opportunity: The company could replace the old infrastructure with equipment that can process iron ore with natural gas or hydrogen instead of coal. Investing in this technology, called direct reduction, would cut the plant’s greenhouse gas emissions by more than 30% if natural gas is used. Using green hydrogen would slash emissions even more, the Industrious Labs team found.

The alternative is to just reline the furnace, which was the course Cliffs chose for the Cleveland facility’s Blast Furnace #5 in 2022.

Relining might provide small emissions cuts when measured per ton of steel, due to increased efficiencies, Lewis said. But ramped-up production from running more ore through the furnace could offset those reductions or even increase total emissions.

Cliffs did not respond to Canary Media’s repeated requests for comment for this story, and it has not yet publicly announced its plans for Blast Furnace #6.

To put itself on track with Cleveland’s emissions goals, however, the company would need to do more than just convert Blast Furnace #6 to the direct reduction process, Industrious Labs said.

The next step in the road map the group laid out would be for Cliffs to process refined iron ore into steel with an electric arc furnace — which can run on carbon-free power — instead of using the current basic oxygen equipment. Investing in green-hydrogen-based direct reduction and an electric arc furnace, instead of relining Blast Furnace #6, would increase emissions cuts to 47%, according to the Industrious Labs report.

Later steps would use direct reduction of iron and an electric arc furnace to refine and process the ore that is currently handled by Blast Furnace #5. Completing that work would cut Cleveland Works’ greenhouse gas emissions by 96%, according to the report.

The Industrious Labs analysis appears to lay out a credible decarbonization pathway, although not necessarily the only one, said Jenita McGowan, Cuyahoga County’s deputy chief of sustainability and climate. Cuyahoga County, which includes Cleveland, also has a goal of net-zero greenhouse gas emissions by 2050 and is in the process of finalizing the latest version of its climate action plan.

“My question about the paper is how feasible it truly is that Cleveland-Cliffs will deploy it in the near future,” McGowan said. Policy uncertainties at the federal level further complicate matters, she added.

For now, the city and county seem to be taking a pragmatic approach, focusing on achievements to date and encouraging future cuts wherever companies will make them.

But getting to net-zero for the industrial sector “will require more fundamental changes … [which] will take place over decades, rather than over a few years,” Cleveland’s climate action plan says. It also notes that low-carbon steel costs 40% more to produce compared to standard methods, “making it difficult for steelmakers to justify the investment in clean production.”

Cuyahoga County’s draft climate plan highlights Cliffs’ energy-efficiency improvements, including Cleveland Works’ use of some iron from the firm’s direct reduction plant in Toledo, Ohio. Cleveland Works also leverages much of the waste heat from its industrial activities to make electricity. The facility recently boosted that combined-heat-and-power generation by about 50 megawatts, the plan notes. That replaces electricity the plant would otherwise need from the grid, a majority of which still comes from fossil fuels.

Faster emissions reductions are certainly better, McGowan said. But the county also wants to make sure companies can stay in business as they decarbonize — especially Cliffs, one of the largest sources of commerce at the city’s port.

In Lewis’ view, decarbonizing Cleveland Works earlier rather than later would be a smart business move for Cliffs. “I think the biggest thing is staying competitive,” Lewis said.

One of Cliffs’ largest markets is supplying high-quality steel for automobiles, including electric vehicles, she added. In March, Hyundai announced plans to invest $6 billion in a new plant in Ascension Parish, Louisiana, that will produce low-carbon steel. As automakers face global pressure to source cleaner metal, Cliffs could find itself left behind, Lewis suggested.

The Industrious Labs report “opens the door for Cleveland to be a leader in clean steel,” Lewis said. Before that can happen, though, “there’s a lot of work to do.”

Every day, people are invited to buy products and services with supposed climate benefits – whether this be “carbon-neutral flights”, “net-zero beef” or “carbon-negative coffee”.

Such claims rely on “carbon offsets”.

Put simply, carbon offsets involve an entity that emits greenhouse gases into the atmosphere paying for another entity to pollute less.

For example, an airline in a developed country that wants to claim it is reducing its emissions can pay for a patch of rainforest to be protected in the Amazon. This – in theory – “cancels out” some of the airline’s pollution.

It is not just businesses that are relying on carbon offsets. Major economies, too, are investing in carbon offsets as a way to meet their international emissions targets – with offsetting becoming a major talking point at UN climate negotiations.

For its supporters, offsetting is a mutually beneficial system that funnels billions of dollars into emissions-cutting projects in developing countries, such as renewable energy projects or clean cooking initiatives.

But offsetting has also faced intense scrutiny from researchers, the media and – increasingly – law courts, with businesses facing accusations of “greenwashing” over their carbon-offsetting claims.

There is mounting evidence that offset projects, from clean-cooking initiatives to forest protection schemes, have been overstating their ability to cut emissions. One yet-to-be published study suggests that just 12% of offsets being sold result in “real emissions reductions”.

Projects have also been linked to Indigenous people being forced from their land and other human rights abuses.

Decades of countries trading carbon offsets has had a negligible impact on emissions and likely even increased them.

In this in-depth Q&A, Carbon Brief explains what offsets are, how they are being used by businesses and nations, and why they can be a problematic climate solution. The article also explores whether a system, which one expert describes as “deeply broken”, could ever be effectively reformed.

Carbon offsetting allows individuals, businesses or governments to compensate for their emissions, by supporting projects that reduce emissions elsewhere.

In theory, after cutting their emissions as much as possible, offsets can pay for low-carbon technologies or forest restoration to “cancel out” emissions they cannot avoid.

This could also provide support for relatively low-cost climate action in developing countries and facilitate greater global ambition.

But, in practice, offsetting often enables these entities to justify “business as usual” – producing the same volume of emissions while making claims of reductions that rely on offsets.

Carbon offsets are tokens representing greenhouse gases “avoided”, “reduced” or “removed” that can be traded between an entity that continues to emit and an entity that reduces its own emissions or removes carbon dioxide (CO2) from the atmosphere.

While it allows the first group to continue to emit, theoretically, the second must reduce its emissions or sequester CO2 by an equivalent amount.

Offsets are usually calculated as a tonne of CO2-equivalent (tCO2e) and are also described as tradable “rights” or certificates.

The terms “carbon offsets” and “carbon credits” are often used interchangeably, but the key difference lies in the marketplace they are traded in and how they are mandated to deliver on emissions reductions.

There are broadly two types of carbon markets on which offsets can be traded. The first is the “compliance” market, which is regulated and involves emissions reductions that are mandated by law, supported by common standards and count towards national or sub-national targets.

Common examples include cap-and-trade emissions trading schemes, such as the EU Emissions Trading System (ETS), where power plants and factories must submit carbon “allowances” to cover their emissions each year, within an overall “cap” for regulated sectors.

Companies can buy and sell allowances from – and to – each other. In some cases they can also buy approved offsets from external emission-cutting projects to stay within their limits.

Such schemes cover around 18% of global emissions and, according to the Intergovernmental Panel on Climate Change (IPCC), they have contributed to emissions cuts in the EU, US and China.

Nevertheless, there is considerable evidence that many of the external offsets that have fed into these schemes have resulted in negligible emissions cuts. (See: How are countries using carbon offsets to meet their climate targets?)

The second type of carbon market is the largely unregulated voluntary carbon market, where offsets are used by corporations, individuals and organisations that are under no legal obligation to make emission cuts. Here, there is far less oversight and even less evidence of real-world emissions reductions.

(Most available credits are eligible for use on the voluntary market, but only a smaller subset can be used for compliance. Initially, UN and government-backed programmes were for compliance markets and NGO-backed programmes were for the voluntary market, but both types of programme now often cater to both markets.)

The table below shows a sample of offsetting registries and programmes on offer. These bodies “issue” offsets – meaning they confirm that a number of tonnes of CO2 has been cut, avoided or removed by a project.

These credits are then bought and “retired” when an entity wishes to count them towards its voluntary goal or binding emissions target. Once retired, they cannot be used again.

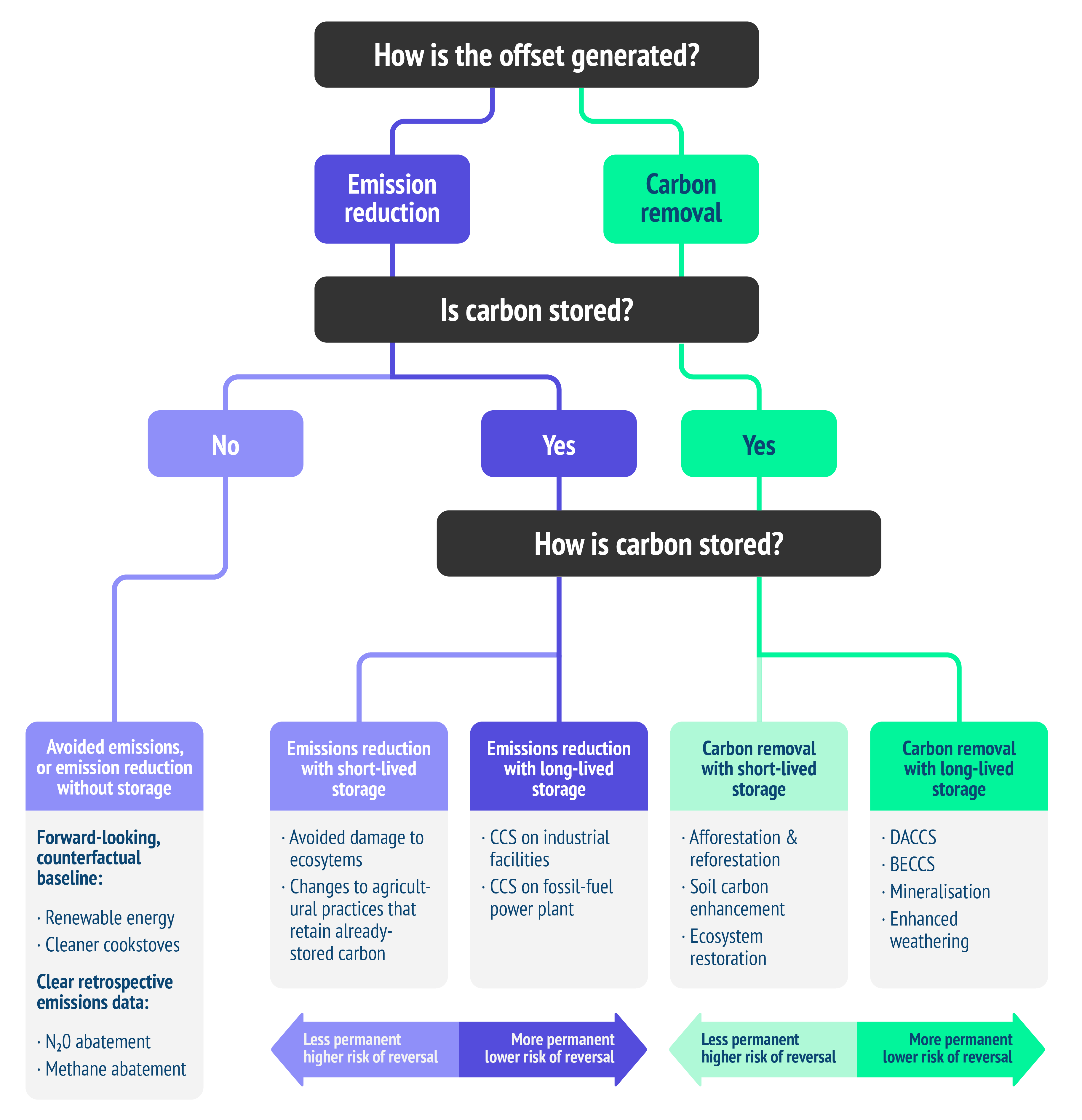

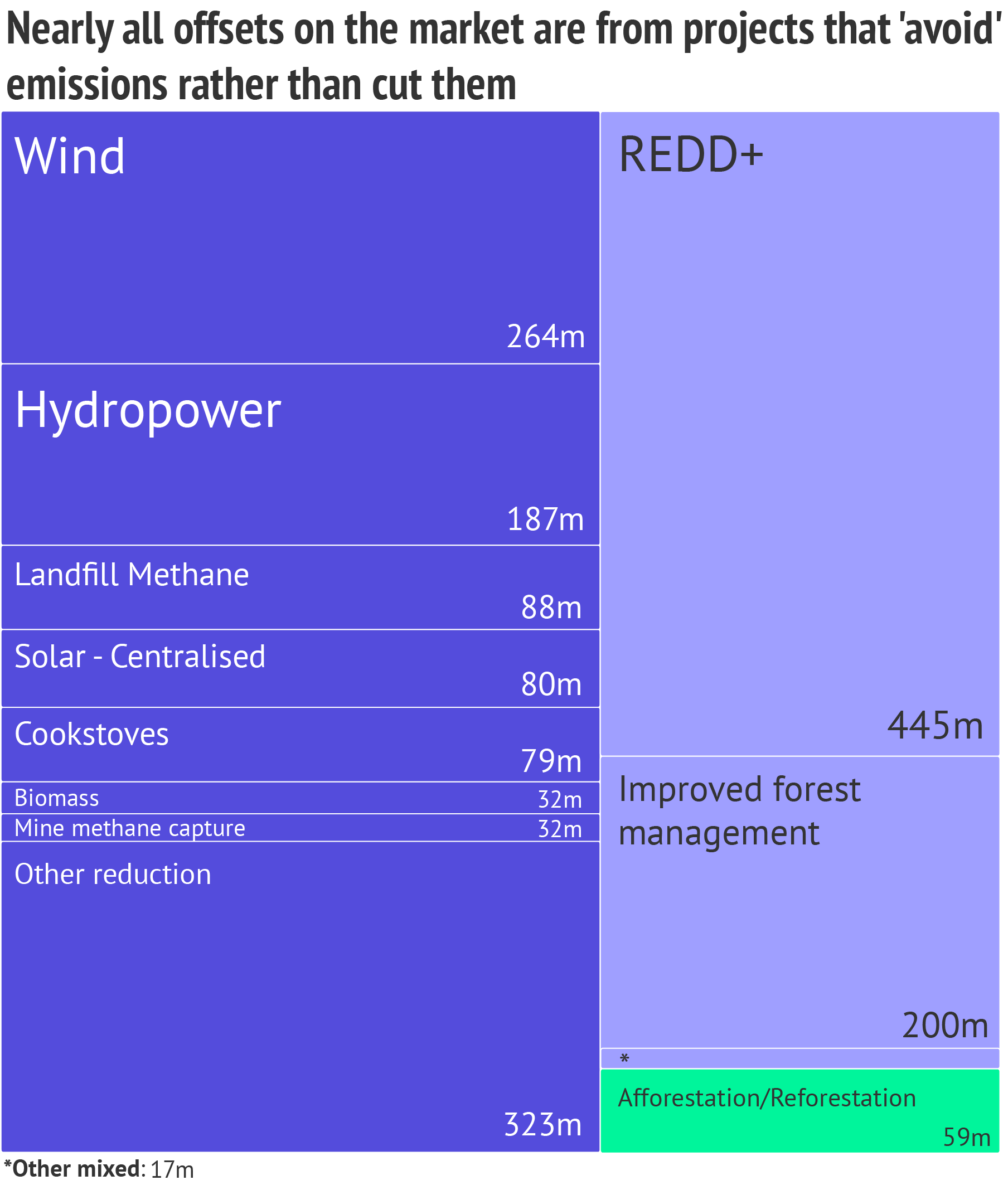

Offsets can broadly be sorted into two groups, which can be seen in the flow chart below, based on the work of the Oxford Offsetting Principles – an academic framework that seeks to define “best practice” for offsetting.

The first group covers “emissions reductions”. These offsets are used when an entity attempts to compensate for an increase in emissions in one area by decreasing emissions in another area. This group of offsets spans a few types, depending on whether emissions are avoided or reduced, with or without storage.

“Avoidance” or “avoided emissions” offsets are from projects that represent emissions reductions compared to a hypothetical alternative. One of the main types of avoidance offsets is renewable projects that are built instead of fossil-fuel plants. Another is “clean” cookstove schemes, where the distribution of more efficient cooking equipment is intended to cut reliance on traditional fuels, such as firewood, leading to lower emissions.

(Note that carbon offsets are a minefield of overlapping terminology and definitions. Here, “avoided emissions” offsets, as defined by the Oxford Offsetting Principles, are distinct from “emissions avoidance” credits, which have a distinct meaning within UN climate talks.)

Emission reduction offsets with short-lived storage of the relevant CO2 include credits from avoided deforestation projects, such as under the framework for reducing emissions from deforestation and forest degradation (REDD+). These are projects that aim to avoid emissions by protecting forests that would have otherwise been cleared or degraded.

(REDD+ was developed at the UN in the late 2000s as a way to help developing countries preserve their forests and is part of the Paris Agreement on climate change. Separately, projects labelled as REDD+ – which may not be aligned with UN rules – have emerged as a major part of the voluntary offset market, accounting for around a quarter of total volumes.)

Adding carbon capture and storage (CCS) technology to a fossil-fuel power plant, meanwhile, could generate emission reduction credits with a longer shelf-life.

“Removals” offsets are generated by projects that absorb CO2 from the atmosphere. Today, most removal offsets involve tree-planting projects, which do not guarantee permanent storage. (See: Could carbon-offset projects be put at risk by climate change?)

A new wave of more permanent removal offsets could be generated using machines that suck CO2 out of the air and techniques such as enhanced rock weathering. So far, these offsets are limited to the voluntary market and are still under review for inclusion in a new international “Article 6” carbon market by the UN.

Taxonomy of carbon offsets with five types of offset based on whether carbon is stored, and the nature of that storage. Diagram by Carbon Brief, based on the original by Eli Mitchell-Larson for the Oxford Offsetting Principle.

According to Carbon Brief analysis of data from the Berkeley Carbon Trading Project, just 3% of offsets on the four largest voluntary offset registries involve removing CO2 – all from tree-planting projects.

Many available offsets have been labelled “junk” or “hot air” because they result from carbon-market design flaws and do not represent real emissions reductions.

The ideas and experiments with carbon offsets and trading trace back at least half a century, as outlined in the timeline below.

Over the years, offset projects have been dogged by allegations of land conflicts, human rights abuses, hampering conservation and furthering coal use and pollution.

They have been decried as a “false solution” by activists. Negotiations over new carbon markets under Article 6 of the Paris Agreement have seen a sustained outcry for not delivering mitigation at scale, threatening Indigenous rights and “carbon colonialism”.

Meanwhile, companies claiming carbon neutrality using voluntary offsets have been increasingly called out and restrained from making “greenwashing” claims. (See: Why is there a risk of greenwashing with carbon offsets?)

The central problem of carbon offsetting is summarised by Robert Mendelsohn, a forest policy and economics professor at Yale School of the Environment. Reflecting on the achievements of carbon offsets, he tells Carbon Brief:

“They have not changed behaviour and so they have not led to any reduction of carbon in the atmosphere…They have achieved zero mitigation.”

Yet with carbon offsets now firmly established, there are still many who view them as an effective way to bolster corporate climate action, encourage governments to pledge more ambitious emissions cuts and channel climate finance where it is most needed.

“I think we can solve the problems that we currently have in the carbon-market space,” Bogolo Kenewendo, a member of the steering committee for the Africa Carbon Markets Initiative, tells Carbon Brief, emphasising the need for “high quality and high integrity credits”.

Since its formation in 1988, the UN’s climate science authority, the Intergovernmental Panel on Climate Change (IPCC), has published six sets of “assessment reports”. These documents summarise the latest scientific evidence about human-caused climate change and are considered the most authoritative reports on the subject.

Prof Joeri Rogelj – director of research at the Grantham Institute – Climate Change and the Environment and professor in climate science and policy at the Centre for Environmental Policy at Imperial College London – has been involved in writing several of these reports.

He tells Carbon Brief that the phrase “carbon offsets” is “not part of the jargon that the [scientific] literature uses”, so it is not widely used in IPCC reports either.

Most carbon-offset projects around today involve “emissions reductions”, whereby an entity can compensate for their pollution by paying for emissions to not happen somewhere else.

This is most commonly achieved by entities supporting, say, the creation of new renewable energy projects in the place of fossil-fuel schemes, for projects that supply clean cookstoves in the global south or for projects that protect ecosystems in order to avoid more deforestation. (More on this in: What are ‘carbon offsets’?)

While IPCC reports do not say much on carbon offsets, they do discuss the role that these kinds of techniques could play in helping the world meet its climate goals.

For example, the latest IPCC report on how to tackle climate change says that all scenarios for limiting global warming to either 1.5C or 2C involve “greatly reduced” fossil fuel use and a transition to low-carbon sources of energy, such as renewables.

It also says that changes to land-use, such as stopping deforestation, “can deliver large-scale greenhouse gas emissions reductions” – although it adds that this “cannot fully compensate for delayed action in other sectors”.

The report also notes that all scenarios for keeping global warming at 1.5C or 2C require “widespread” access to clean cooking.

A much smaller proportion of carbon offsets around today work by aiming to remove CO2 from the atmosphere to compensate for an entity’s emissions elsewhere.

This is commonly achieved by planting trees, which remove CO2 from the atmosphere as they grow, or by restoring damaged ecosystems, which are natural carbon stores.

Other, more technologically advanced types of CO2 removal are being tested and developed by a handful of companies around the world.

These include growing plants, burning them to generate energy and then capturing the resulting CO2 emissions before they reach the atmosphere – a technique called bioenergy with carbon capture and storage (BECCS).

Another proposed technique would be to use giant fans to suck CO2 straight from the atmosphere before burying it underground or under the sea – a technology called direct air capture and storage (DACCS).

However, neither one of these technologies exist at scale at present – and, therefore, do not yet play a large role in carbon offsetting.

The latest IPCC report on how to tackle climate change concludes that CO2 removal techniques are now “unavoidable” if the world is to limit global warming to 1.5C or 2C.

And Carbon Brief analysis finds that CO2 removal is used to some extent in nearly all scenarios that limit warming to below 2C.

While there is clear scientific evidence that techniques to cut emissions and remove CO2 from the atmosphere will be needed to meet global climate goals, there is not yet a clear understanding of whether finance provided via carbon offsets could – or should – help with implementation.

The latest IPCC report on how to tackle climate change does not discuss in detail the extent to which carbon-offset finance provided by countries could help with implementation, report lead author Dr Annette Cowie, principal climate scientist at the University of New England in Australia, tells Carbon Brief.

One reason for this is that the report was written when countries were still debating the rules for how carbon markets should work under the Paris Agreement, Cowie says. (For more, see: How are countries using carbon offsets to meet their climate targets?)

In addition, the report did not have a “a big focus” on how businesses and organisations use carbon offsets in the voluntary carbon market because the IPCC tends not to focus on the “company level”, she says. (For more, see: How are businesses and organisations using carbon offsets?)

Nevertheless, the report does say that “we will need the private sector to contribute to funding the climate challenge” and refers to carbon markets as a “potentially effective mechanism to achieve this”, she adds.

Nearly every country in the world has set out plans under the Paris Agreement to cut its emissions. Most major economies also have net-zero targets.

Nations have also agreed on a succession of carbon-offset programmes, overseen by the UN. These systems could, in theory, help identify the cheapest emission cuts and enable those countries struggling with their climate goals to pay for reductions elsewhere.

This could help governments achieve their targets and encourage them to set more ambitious ones. It could also deliver money to developing countries, where much of the low-hanging fruit is located – but financial support is needed to take advantage of it.

Yet, despite being in operation for around two decades, so far these mechanisms have not driven a tangible reduction in countries’ emissions.

Instead, energy companies and factories in large, emerging economies have made money selling cheap, but often worthless, offsets to developed countries. As a result, these programmes have increased global emissions.

The earliest major offset schemes were established with the Kyoto Protocol – the first binding international agreement to cut emissions – in 1997.

By far the largest was the Clean Development Mechanism (CDM). This is a compliance mechanism that has allowed developed countries to meet their binding Kyoto emissions targets by buying credits largely generated by low-carbon energy projects in developing countries.

Souparna Lahiri, climate policy advisor with the Global Forest Coalition and a critic of carbon markets, tells Carbon Brief the CDM gave “leeway” to developed countries:

“[They said] let’s spend money where you can reduce [emissions] at a much cheaper cost. So we don’t spend much, but in return for investing…we get a credit that we can balance out with our own emissions.”

The CDM was also meant to channel much-needed climate finance to developing nations, which were not obliged to cut their own emissions under the Kyoto Protocol.

Carbon Brief analysis of UNFCCC data shows China, India, South Korea and Brazil account for 81% of the CDM credits that have been issued, with China alone issuing more than half, as the chart below shows. Barring Egypt and South Africa, African nations have issued just 1% of the credits on the market.

The CDM was agreed alongside another offsetting strategy, termed “Joint Implementation”,

The EU, New Zealand and Switzerland allowed their power plants and factories to purchase Kyoto credits to meet their emissions trading system (ETS) (As of 2020, CDM credits were no longer eligible for use under the EU ETS.)

According to one study, the Kyoto markets helped nine developed countries, including Japan, Spain and Switzerland, meet their initial targets.

Despite this apparent success, many have concluded that the CDM has, ultimately, hindered rather than helped global climate action.

This is because most of the low-carbon projects it supported would likely have happened without finance from developed countries, either because they were already profitable or required by law.

A 2016 EU-commissioned study concluded that 85% of CDM projects, particularly wind power and hydropower plants, were likely to have overestimated their emissions reductions and supported no “additional” low-carbon capacity in developing countries. According to the IPCC’s AR6 report:

“There are numerous findings that the CDM, especially at first, failed to lead to additional emissions cuts in host countries, meaning that the overall effect of CDM projects was to raise global emissions.”

One study found the CDM may have increased emissions by 6bn tonnes of CO2 (GtCO2).

Reports began to emerge in 2012 that the CDM market had “collapsed” amid a “carbon panic”. This was largely the result of a lack of demand from the EU ETS.

From 2012, the EU decided to limit the credits it would accept under the scheme – for example, excluding those generated by industrial gas cuts in factories. Such CDM projects had been accused of incentivising the additional production of greenhouse gases in order to claim credits for destroying them.

The EU also stopped accepting new credits unless they came from least developed countries. At the same time, other developed countries failed to set more ambitious Kyoto targets, meaning there was little demand from outside the EU.

(Despite pushing hard for the inclusion of carbon offsetting, the US ended up not participating in the Kyoto Protocol at all, removing a key potential market for credits.)

The credit price slumped from a record high of $27.50 per tonne of CO2 in 2008 to $0.55 per tonne in 2012. As the chart below shows, the number of new projects being registered to participate in the CDM fell dramatically and has never recovered (although projects continue to issue credits to this day).

With the Paris Agreement, countries agreed to establish new carbon markets that would ultimately replace the troubled Kyoto system. They are collectively known as Article 6 markets, referring to the section of the treaty laying out how countries could “pursue voluntary cooperation” to reach their climate targets.

The carbon-trading components include Article 6.2, which enables countries to directly trade credits dubbed Internationally Transferred Mitigation Outcomes (ITMOs) with each other, and Article 6.4, which creates a new, UN-backed carbon market to effectively replace the CDM.

Unlike the CDM, any country – developed or developing – can buy and sell credits using Article 6 mechanisms to meet their climate goals under the Paris Agreement.

Critically, the new carbon market established under Article 6.4 – but not Article 6.2 – includes a specific goal to “deliver an overall mitigation in global emissions”, achieved by automatically cancelling 2% of any credits that are traded in this system.

This should mean that offsetting under this system is no longer a zero-sum game. No one will be allowed to use those 2% of credits to claim an emissions reduction, ensuring a real-world drop rather than simply moving emissions cuts from one place to another.

Nations have also agreed to avoid “double-counting” Article 6 credits, meaning that if an offset is sold by one country to another, they cannot both count its emissions cuts towards their climate targets. (See: Why is there a ‘double-counting’ risk with carbon offsets?)

Negotiations over the technical details of these new markets have been lengthy and complex.

Some details are still being hashed out by an Article 6.4 supervisory body and the trade in credits under this system is not expected to start until 2024 at the earliest, once the final rules have been established.

Among the issues at stake in the body’s various meetings are methodologies for calculating how many credits are issued and whether to include carbon-removal projects.

Some initial agreements to exchange ITMOs under Article 6.2 have already been made between a handful of nations, including Switzerland with Peru and Ghana.

(See Carbon Brief’s in-depth explainer on the background and technical elements of Article 6 carbon markets, plus the overviews of COP25, COP26, COP27 and the most recent UN talks in Bonn, for details of how these markets have been negotiated.)

According to the International Emissions Trading Association (IETA), 156 countries have signalled their intention to use Article 6 markets either as buyers or sellers. It estimates that the markets could trigger billions of dollars in climate investment and reduce the total cost of implementing climate plans by $250bn a year by 2030.

(IETA represents the carbon-trading sector, including fossil-fuel companies, which have broadly supported market-based approaches in UN climate negotiations.)

Pedro Chaves Venzon, international policy advisor at IETA, tells Carbon Brief:“I expect rapid growth of engagement with Article 6 in the coming years…because not all countries have the potential to scale emission reductions and removals to achieve net-zero only through domestic action.”

Yet supply and demand for Article 6 credits is not guaranteed.

Unlike the Kyoto Protocol, the Paris Agreement requires every country to make an emissions-cutting pledge, not just developed countries.

The avoidance of double-counting could, therefore, make it difficult for countries to both sell large numbers of offsets and also meet their emissions goals. Scott Vaughan, senior fellow at the International Institute for Sustainable Development (IISD), tells Carbon Brief.

“It’s really important for sellers to beware, particularly for developing countries, because you don’t want to be in a position where you end up essentially selling your low-hanging fruit… [then having] very few options in terms of your own domestic [goals].”

Moreover, IETA’s assumptions about nations buying and selling credits are based on governments having more ambitious plans to cut emissions than they do today. If climate goals are not ramped up, there will be less pressure to buy emissions offsets from others.

Finally, civil society groups are concerned that Article 6 markets could repeat the same mistakes as the CDM.

Following years of argument, a relatively small number of CDM credits issued during 2013-2020 are eligible for use to meet nations’ 2030 climate pledges under the Paris Agreement.

(Australia had long proposed to use such credits to meet its Paris pledge. In 2020, following years of pressure, it climbed down and agreed to meet its pledge through domestic action.)

In addition, CDM projects will be allowed to continue issuing credits under the new system, if they meet the new Article 6.4 rules. This could lead to billions of what Carbon Market Watch calls “largely dud credits” entering the Paris regime, with one analysis estimating that up to 2.8bn carbon credits could be issued.

Businesses and other organisations are turning to carbon offsets in response to growing pressure to act on climate change, either to meet legal targets or their own, self-assigned emissions goals.

More than half of the world’s largest 100 companies by revenue have said they intend to purchase offsets, according to Carbon Brief analysis of Net Zero Tracker data. Only four have expressly ruled them out – Walmart, Brookfield Asset Management, Roche and Thai oil-and-gas company PTT Exploration & Production.

Among the biggest offset users are large oil-and-gas companies, airlines and car manufacturers.

In theory, “best practice” for businesses using offsets would involve them cutting their emissions as much as possible each year. Then, offsets could be purchased from elsewhere to cover any “residual” emissions that are too difficult or costly to reduce.

Yet there have been many accusations of “greenwashing” as firms buy cheap offsets of questionable quality, often from projects in developing countries, rather than doing their best to cut their own emissions. (See: Why is there a risk of greenwashing with carbon offsets?)

In places such as the EU, California and Quebec, high-emitting businesses, including factories and power plants, can purchase compliance offsets to meet their legal emissions-cutting obligations under regional emissions trading schemes. These schemes cover billions of tonnes of emissions – and some have linkedemissions cuts at participating facilities to the impact of the regulations.

The UN Carbon Offsetting and Reduction Scheme for International Aviation (Corsia) is a unique example where an entire sector will be obliged to purchase carbon credits to offset its emissions growth beyond 2027.

Beyond such legal requirements, businesses have faced growing societal demand for climate action, corporate social responsibility and the uptake of net-zero pledges.

An entire market has sprung up to serve this demand, known as the voluntary offset market. It is largely unregulated and frequently described as a “wild west” full of “junk” credits.

The voluntary market is underpinned by standards and registries such as the Verified Carbon Standard (VCS) – light blue in the chart below – which accounts for nearly two-thirds of the voluntary market and is administered by the NGO Verra.

The chart below, which shows the number of credits issued by different registries each year, demonstrates the growing dominance of these standards (shades of purple) compared to the UN’s Clean Development Mechanism (CDM – green).

Number of offset credits issued, millions, in the four largest voluntary offset registries, American Carbon Registry (ACR), Climate Action Reserve (CAR), Gold Standard and the Verra (VCS), as well as credits issued by those registries and used for compliance under the California Air Resources Board cap-and-trade programme (shades of purple). Credits issued under the UN-backed Clean Development Mechanism (CDM) are shown in green. Source: Berkeley Carbon Trading Project. Chart: Carbon Brief.

It demonstrates how demand has grown beyond companies and countries investing in CDM offsets solely to meet their obligations under emissions trading schemes and the Kyoto Protocol. (For more on the CDM, see: How are countries using carbon offsets to meet their climate targets?)

Unlike UN-backed credits, the organisations issuing these voluntary market offsets are NGOs and private entities. They have their own frameworks for verifying and issuing credits.

(The division between “voluntary” and “compliance” markets is complicated by the fact that businesses can also buy compliance offset market credits – for example, from the CDM – to make voluntary claims, if they wish. At the same time, compliance programmes such as Corsia or California and Quebec’s cap-and-trade scheme

allow participants to purchase an approved subset of voluntary offset credits to meet compliance targets. Credits issued for the latter scheme are indicated by the California Air Resources Board section of the chart above.)

On top of the standards, there is a supporting ecosystem of auditors who check that offset projects are working as they are supposed to, as well as exchanges and retailers who trade in offsets and act as middlemen in transfers. The infographic below outlines the steps involved in the production, certification and sale of offsets, along with problems that can occur along the way.

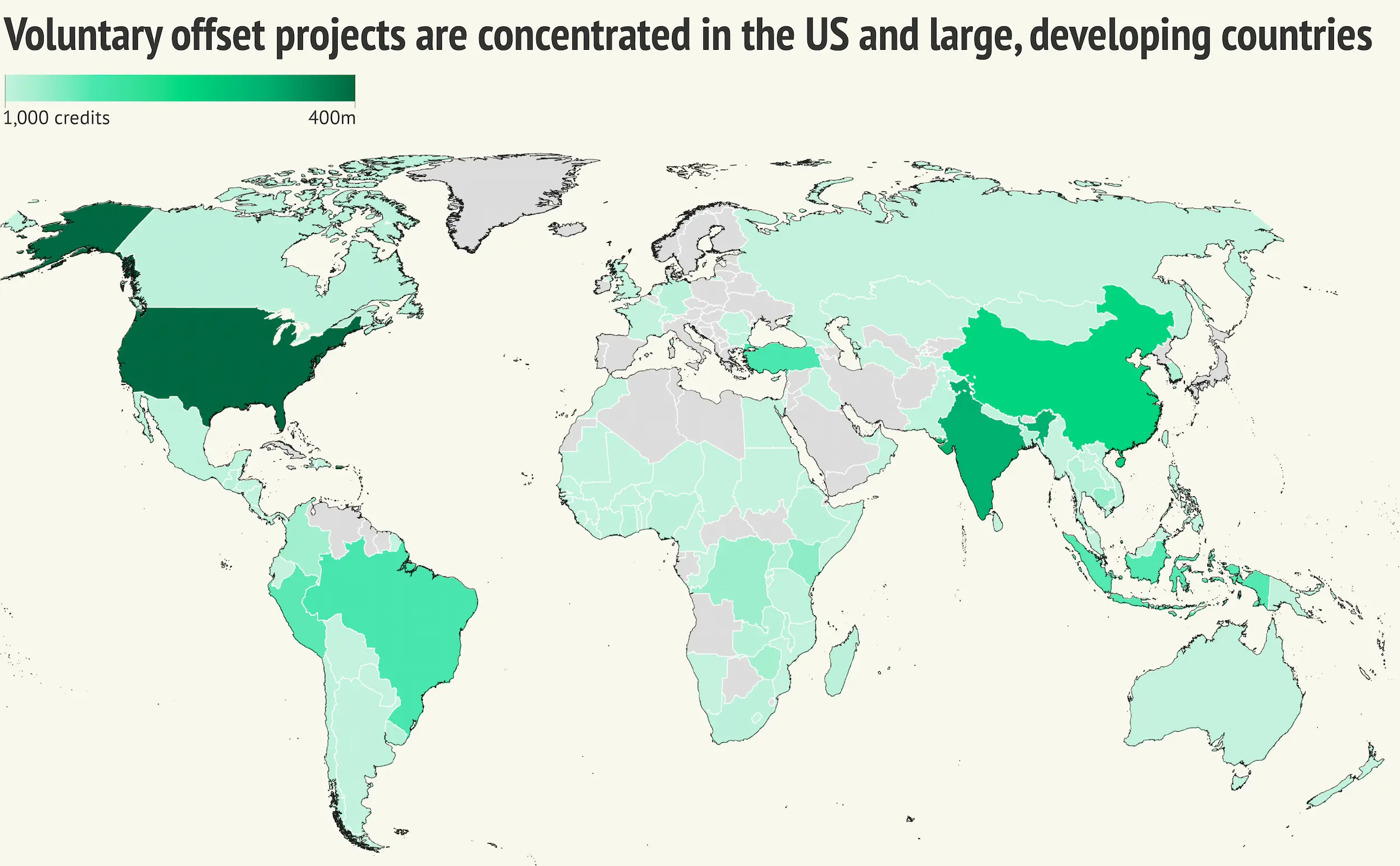

According to Carbon Brief analysis of data collected from the four largest voluntary offset project registries by the Berkeley Carbon Trading Project, three-quarters of the 1.8bn voluntary offsets issued are from projects in developing countries, as the map below shows.

As with the CDM, large, emerging economies, such as China and India, have generated a lot of these credits, with 16% and 12% of the total, respectively. As have countries with sizable forests, such as Peru and Indonesia.

Nearly all of the remaining credits are from the US, which is the largest issuer. However, roughly 90% of its credits come from primarily US-based registries, such as the American Carbon Registry, which are, in turn, largely purchased by US-based organisations – often to meet legal targets.

Number of offset credits issued on the four largest voluntary offset registries, American Carbon Registry (ACR), Climate Action Reserve (CAR), Gold Standard and Verra (VCS), by country. Source: Berkeley Carbon Trading Project. Map: Carbon Brief.

A report released by Shell and Boston Consulting Group found the voluntary offset market reached a record $2bn in 2021, four times larger than the previous year. It estimated the market would reach $10-40bn in value by 2030 – and many players in the sector have projected “exponential” growth for voluntary offsets in the coming years.

(This is still far smaller than the value of “carbon markets” more broadly. The trading of permits on the EU ETS and other regional emissions trading schemes was valued at $851bn in 2021.)

There is a disconnect between predictions of growth and the recent backlash against the voluntary offset market.

Prices of voluntary carbon offsets have plummeted over the past year. Investors have been hit by the economic downturn, but there are also broader concerns about the integrity of voluntary offsets. Dr Barbara Haya, director of the Berkeley Carbon Trading Project, tells Carbon Brief:

“The market is in a lot of flux right now and there are two factors pulling in opposite directions where you have all of these carbon-neutral and net-zero targets. So there’s growing interest from buyers to buy offsets, but then also a growing realisation that the market is deeply broken and almost all credits are over-credited.”

(For more on why most offsets are over-credited, see: Do carbon-offset projects overestimate their ability to reduce emissions? and Why is there a ‘double-counting’ risk with carbon offsets?)

Such issues have led to the Science Based Targets Initiative, an organisation that sets guidelines for corporate climate policy, stating unambiguously:

“The use of carbon credits must not be counted as emission reductions toward the progress of companies’ near-term or long-term science-based targets.”

At the same time, Haya adds that offsets can help to promote emissions reductions within businesses.

“Many companies would not have taken on carbon-neutrality goals if it weren’t for that option to buy cheap carbon credits,” she says. Analysis by carbon credit-rating company Sylvera found companies that were investing in offsets were simultaneously cutting their actual emissions at twice the rate of companies that were not.

Efforts to improve the market (see: Is there a way for carbon offsets to be improved?) are underway and Pedro Chaves Venzon, from industry group IETA, tells Carbon Brief that the voluntary market could also help develop methodologies and quality standards for use in international compliance markets:

“While they may not be perfect, they can play a key role in the planet’s journey to net-zero as they can help governments to build the infrastructure required for countries to develop compliance systems and engage with Article 6.”

In conclusion, Haya tells Carbon Brief: “I think it’s absolutely essential that we fix quality before growing the market, otherwise you have an even bigger market standing on a house of cards which is going to collapse when there’s scrutiny.”

One major criticism of carbon offsetting schemes is that they can often, for various reasons, overstate their ability to reduce emissions.

This can be intentional or unintentional. (For more on intentional efforts to overstate the benefits of carbon offsets, see: Why is there a risk of greenwashing with carbon offsets?)

Understanding the ways in which carbon-offset projects can overestimate their ability to cut emissions is important.

This is because, by design, carbon offsets do not lead to a net reduction in emissions entering the atmosphere – but rather aim to allow an entity to “cancel out” their pollution by paying for another entity to pollute less. If the entity paid to pollute less has overestimated its ability to do so, it will lead to a net increase in emissions, exacerbating climate change.

Most carbon-offset projects around today involve “emissions reductions”, whereby an entity can compensate for its pollution by paying for emissions to not happen somewhere else.

This is most commonly achieved by entities subsidising, say, the creation of new renewable energy projects in the place of fossil fuel schemes, supporting projects that supply clean cookstoves in the global south or projects that protect ecosystems in order to avoid more deforestation. (More on this in: What are ‘carbon offsets’?)

Each of these approaches come with risks, says Gilles Dufrasne, global carbon markets lead at the independent watchdog Carbon Market Watch. He tells Carbon Brief:

“For all three you have strong scientific evidence on how there is a massive risk of overestimation in terms of the impacts that these projects are having.”

A recent preprint – a study that has not yet completed the peer review process – estimated that just 12% of carbon-offset projects around today “constitute real emissions reductions”.

There are several ways in which overestimates of emissions reductions can occur.

The first comes from the way that projects measure their ability to reduce emissions, says Dufrasne:

“The big problem with these projects is setting the baseline. When you measure the impact of your project, what are you comparing it to? You’re comparing it to what would have happened in the absence of your project. That counterfactual is quite difficult.”

For example, a forest protection project will generate a certain number of carbon credits to sell on to polluters based on how much deforestation the project developers think they have stopped from happening.

Research shows that forest protection schemes often overestimate how much deforestation they have prevented – and, thus, the amount of emissions they have been able to offset.

One study examining 12 forest protection projects in the Brazilian Amazon found that they consistently overestimated how much deforestation they had prevented.

An investigation by the Guardian, the German weekly Die Zeit and SourceMaterial, a non-profit investigative journalism organisation, published earlier this year found that 90% of the rainforest protection schemes approved by Verra, the world’s largest carbon offsets standards agency, had grossly overestimated the amount of emissions they had saved. Verra strongly refuted the allegations.

An analysis by carbon credit ratings agency Calyx Global found that 70% of clean cookstove projects significantly overestimated their ability to reduce emissions.

And a separate investigation by the Guardian published in September found that the majority of carbon-offset projects that have sold the most carbon credits did not deliver on promised emissions reductions.

Another way that overestimates occur comes from assumptions about how long offset projects can keep carbon locked up. This concept is often called “permanency”.

During a transaction, buyers purchase credits – each representing one tonne of CO2 – with the assumption that an equivalent amount of carbon will be offset somewhere else.

However, this transaction does not consider whether the amount of CO2 offset will stay out of the atmosphere permanently.

This is particularly a problem for forest protection schemes, Dufrasne explains:

“The CO2 you’re emitting into the atmosphere when you burn fossil fuels is going to stay there for centuries to millennia, but the carbon stored in forests – we don’t know how long that is going to stay there. So, there is no equivalence between storing carbon in forests and avoiding the combustion of fossil fuels.”

The carbon stored inside forest protection schemes is at risk from myriad factors.

This includes political and economic changes, which may affect deforestation rates, as well as climate change, which is making tree-killing events, such as wildfires and droughts, more likely. (See: Could carbon-offset projects be put at risk by future climate change?)

This “permanency” risk is well illustrated when a fossil-fuel company pays for its emissions to be offset by a forest-protection scheme, says Dufrasne: