Canary Media’s chart of the week translates crucial data about the clean energy transition into a visual format.

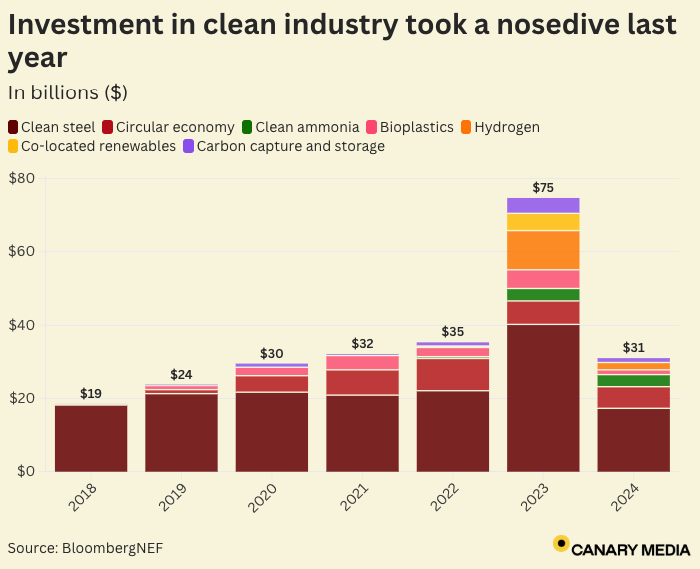

Global investment in efforts to decarbonize heavy industries totaled just $31 billion in 2024, marking a tough year for areas including hydrogen-based steelmaking and carbon capture and storage.

Money for clean industry–related projects fell by nearly 60% last year compared with 2023 — even as investment in the broader energy transition grew to a record $2.1 trillion in 2024, per BloombergNEF.

The diverging outcomes reflect a “two-speed transition” emerging in markets around the world, according to the research firm. The vast majority of today’s energy-transition investment is flowing to more established technologies, such as renewable energy, electric vehicles, energy storage, and power grids.

Meanwhile, efforts to slash planet-warming emissions from heavy industrial sectors — including steel, ammonia, chemicals, and cement — continue to face more fundamental challenges around affordability, maturity, and scalability.

Clean steel projects took the biggest hit in financial commitments, with investment falling to around $17.3 billion in 2024, down from $40.2 billion the previous year, BNEF found.

The category includes new furnaces that can use hydrogen instead of coal to produce iron for steelmaking. Green hydrogen made from renewables remained costly and in scarce supply, leading producers like Europe’s ArcelorMittal to delay making planned investments in hydrogen-based projects. Electric arc furnaces — which turn scrap metal and fresh iron into high-strength steel using electricity — are also considered clean steel projects. Mainland China saw a sharp decline in funding for new electric furnaces as steel demand withered among its automotive and construction industries.

Investment held flat in 2024 for new facilities that use “low-emissions hydrogen” instead of fossil gas to produce ammonia, a compound that’s mainly used in fertilizer but could be turned into fuel for cargo ships and heavy-duty machinery. However, funding declined last year for circular economy projects that recycle plastics, paper, and aluminum, as well as for bio-based plastics production.

BNEF found that, unlike in 2023, few developers of new clean steel and ammonia facilities allocated capital for “co-located” hydrogen plants and renewable energy installations. Likewise, fewer commitments were made to install carbon capture and storage units on polluting facilities like cement factories and chemical refineries.

Whether these investment trends will continue in 2025 depends largely “on a few crucial policy developments in key markets,” Allen Tom Abraham, head of sustainable materials research at BNEF, told Canary Media.

In the United States, companies are awaiting more clarity on the future of federal incentives for industrial decarbonization. The Biden administration previously directed billions of dollars in congressionally mandated funding to support cutting-edge manufacturing technologies and boost demand for low-carbon construction materials — money that is now entangled in President Donald Trump’s federal spending freeze.

Investors are also watching to see what unfolds this month in the European Union. Policymakers are poised to adopt a “clean industrial deal” to help the region’s heavily emitting sectors like steel, cement, and chemicals to slash emissions while remaining competitive. And in China, the government is drafting new rules aimed at easing the country’s overcapacity of steel production, which could impact the deployment of new electric arc furnaces.

“Positive developments on these initiatives could boost clean-industry investment commitments in 2025,” Abraham said.

.svg)